It’s the Land, Stupid!

Rethinking Economics, 2020

Pluralist Showcase

In the pluralist showcase series by Rethinking Economics, Cahal Moran explores non-mainstream ideas in economics and how they are useful for explaining, understanding and predicting things in economics.

![]()

It’s the Land, Stupid!

By Cahal Moran

In this episode of the pluralist showcase series, we are going to look at Georgism, a term for a worldview founded by Henry George, an economist and philosopher from the late 19th Century. The core of Georgism is a policy known as the Land Value Tax (LVT), a policy which Georgists claim will solve many of society and the economy’s ills. Georgism is an interesting school of thought because it has the twin properties that (1) despite a cult following, few people in either mainstream or (non-Georgist) heterodox economics pay it much heed; (2) despite not paying it much heed, both mainstream and heterodox economists largely tend to agree with Georgists. I will focus on the potential benefits Georgists argue an LVT will bring and see if they are borne out empirically. But I will begin by giving a nod to the compelling theoretical and ethical dimensions of George’s analysis, which are impossible to ignore.

Why Tax Land?

Both the ethical and economic reasoning behind taxing land rest on one disarmingly simple insight: land cannot be produced. As a result, nobody is naturally entitled to it and taxes cannot discourage its production. What’s more, increases in the value of land are unearned, since when an area is more desirable it is a result of the collective efforts of the community rather than the individual efforts of the landowner. Leafing through Henry George’s magnum opus, Progress and Poverty, he makes this point beautifully. He is also extremely careful with his definitions and logic, and for these reasons is worth quoting at length:

“The term land necessarily includes, not merely the surface of the earth as distinguished from the water and the air, but the whole material universe outside of man himself, for it is only by having access to land, from which his very body is drawn, that man can come in contact with or use nature. The term land embraces, in short, all natural materials, forces, and opportunities, and, therefore, northing that is freely supplied by nature can be properly classed as capital.”

It is, he says, inherently unjust to own land:

“The right to exclusive ownership of anything of human production is clear. No matter how many the hands through which it has passed, there was, at the beginning of the line, human labor – some one who, having procured or produced it by his exertions, had to it a clear title as against all the rest of mankind, and which could justly pass from one to another by sale or gift. But at the end of what string of conveyances or grants can be shown to or supposed a like title to any part of the material earth?”

It is hard to argue with this point, though in typical 19th century style George belabours it over tens or even hundreds of pages. I found myself yearning for some more concrete analysis and especially evidence of any sort but by the time I gave up reading it hadn’t appeared. (If evidence does appear in the book, I am happy to be corrected on this point.)

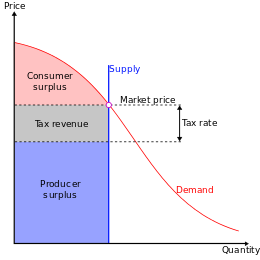

One of the most counterintuitive claims made for an LVT is that it won’t increase the price of land. Georgists argue that it can’t be passed on because land owners are forced to pay it no matter what they do with the land so it doesn’t affect their incentives. Neoclassical economists agree with this, and the logic is best illustrated with a supply and demand diagram as below:

Because the supply of land is fixed - excepting some crimes against nature in Dubai – the tax cannot be passed on as would any other. The original price is at the dot at the crossover between demand and supply and does not change with the introduction of the tax, which is taken entirely out of ‘producer surplus’ aka the landlord’s rents. As with every argument for the land tax this logic is compelling, but we need to check it with evidence to be sure.

Land Value Taxes: the Evidence

The market for property and houses faces a number of deep-seated problems which have consequences for people and for the rest of the economy, including but not limited to:

- High house prices and rents;

- Huge geographic inequality in prices and rents;

- Recurrent bubbles and busts;

- Urban sprawl;

- Lack of availability;

- Un(der)used land;

Georgists would claim an LVT would help with or even solve most of these. Since land taxes have been implemented in more than 30 countries around the world, we can ask whether their claims are borne out.

One consistent empirical finding is that land taxes lead to higher levels of building. Sally Kwak and James Mak detail Hawaii’s experience when they introduced a land tax in 1963 - income went from 20% below the national average in 1959 to 25% above the national average in 1970. Although this point does not meet modern empirical standards for identifying causality, it is notable that the tax was largely abandoned in 1977 primarily because officials perceived it as having resulted in too much growth, with its critics citing environmental concerns about high density building. Apparently Joni Mitchell’s “they paved paradise and put up a parking lot…” was inspired by this very problem! Pittsburgh, Pennsylvania had a similar, albeit more positively perceived experience after near-quadrupling its land tax relative to other cities nearby in 1980. According to Oates and Schwab it was “the only city to have experienced a large and significant increase in levels of building activity during the 1980s”, despite being on a downward trend (along with the rest of Pennsylvania) before the tax. They run regression analysis to rule out alternative explanations, though it is unsophisticated by modern standards.

This finding actually points to a common criticism of LVTs which is missed by the type of static model described above: as they are levied no matter what the land owner does, they can be thought of as a tax on waiting and so they may cause investors to frontload building decisions, leading to excess and waste. Oates and Schwab argue that if the LVT is properly estimated it need not lead to excess building, though in my opinion this begs the question of how to estimate “properly” (they even note later on that “the determination of assessed land-values is more complex and pragmatic than the discussion to this point would suggest”). There is also the point, made by Dye and England, that if land owners cannot afford the tax one year – or borrow to cover it – this will push their decisions forward no matter the efficacy of the estimation. On the other hand, this process could be argued to reduce speculation.

The evidence is scanter, less rigorous and more conflicting for the other benefits of the LVT claimed by Georgists. For example, a decade or so ago there were a couple of papers in the National Tax Journal which used simulations to look at the inherent progressivity of land value taxes as opposed to other taxes in the US. England and Zhao studied Dover in New Hampshire and found that moving to land taxes from property taxes hurts the poor more because their properties are worth less relative to their land than the rich, who benefit from a reduction in taxes on their luxury housing. Conversely, the second paper by Bowman and Bell studies Roanke in Virginia and finds that the tax benefits those on average and low incomes, which they attribute to different demographics and tax base compared to Dover. As for the claim that land taxes will reduce speculation, I could find only one paper with suggestive evidence from Ontario, Canada that land taxes abet rises in house prices.

A couple of other papers have used more rigorous methods to determine the success of the LVT in achieving its goals. One 2009 paper by Banzaf and Lavrey compared counties with different levels of land taxes across Pennsylvania. Consistent with the other evidence, the authors found that construction rates, number of rooms per person, and density all increased as a result of higher land taxes. A recent working paper by Murray and Hermans uses similar methods to show that in Victoria, Australia land taxes are both more progressive and effect more building than standard property taxes. I would like to see more papers like these two from Georgists, and to be frank I think it’s an open goal for young economists (maybe even myself) to use modern techniques to test each and every one of the purported benefits of land value taxes.

Summing Up

Like so many adherents to one school of thought, Georgists are prone to overstating their case. The confidence with which the 10 advantages of the land value tax listed on the website http://www.landvaluetax.org outstrips the depth of the empirical evidence for most of them. I am confident in saying that a land tax is just; that it will spur growth and reduce urban sprawl; and that it is a practical way to raise revenue. However, I am not as confident in its progressivity, its ability to reduce speculation, and the idea that it cannot be passed on to tenants. In defence of George, he advocated a 100% tax and current values are far, far short of this. This makes identifying the effects difficult, both because they may not surface at low levels of taxation and because statistical identification relies on more variation than many cases give us. Overall, the LVT is a good idea which will certainly do no harm, but which is sometimes oversold as a great idea which will fix all our woes.

There is still so much to discover!

In the Discover section we have collected hundreds of videos, texts and podcasts on economic topics. You can also suggest material yourself!