Taxation in the MENA region

Pluralist Economics Fellowship, 2018

This dossier is part of the Pluralist Economics Fellowship, jointly put together by the Minerva Schools at KGI & The Network for Pluralist Economics. For more information on this and a collection of the other student essays check out this page.

Taxation in the MENA region

Author: Sanchita Shekar

Review: Prof. Robson Morgan

Table of Contents

What can the MENA region do with additional Tax

A Case Study: Georgia Tax Collection System

Proposed Solutions: Export Diversification

Abstract

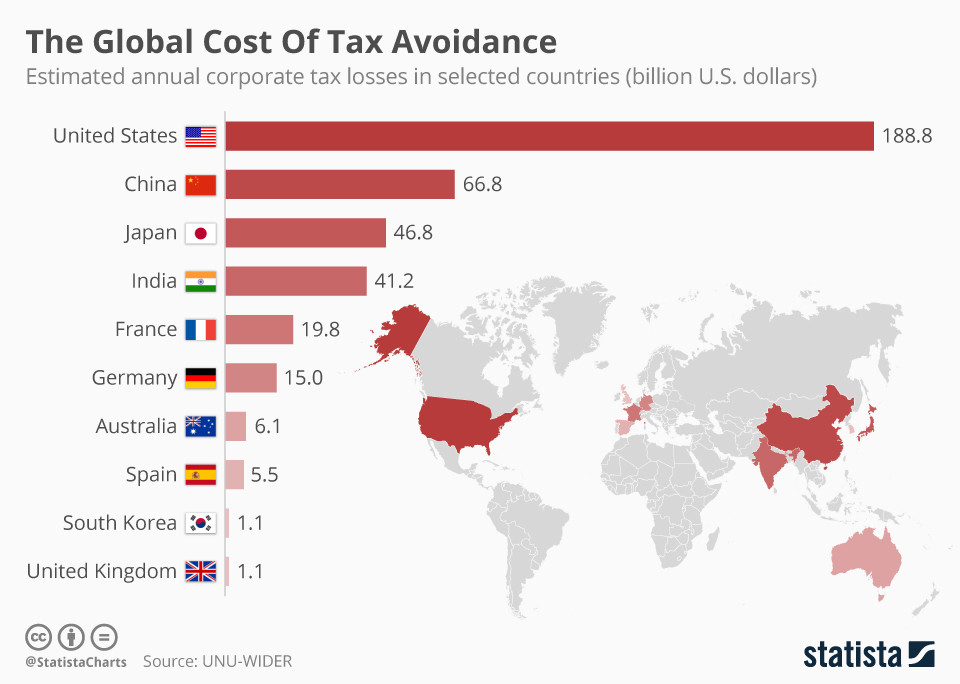

While increased tax revenue can increase government earnings if collected efficiently, there is a global trend towards lower corporate taxation to prevent profit shifting and cross-border adjustments for multinational corporations (MNC) (cited in Riskjell, 2014). The lower corporation taxes function as incentives for MNCs to pay taxes within the region of operation rather than engaging in illicit financial practices such as tax evasion and profit shifting. However, having low tax rates has served the hydrocarbon focused Middle East and North African (MENA) region well historically, and tax avoidance isn’t as significant an issue in the MENA region as it is in the United States and China (See Exhibit 1).

Exhibit 1: The Top 10 Countries with the highest Annual Corporate Tax Losses. Source: Statista

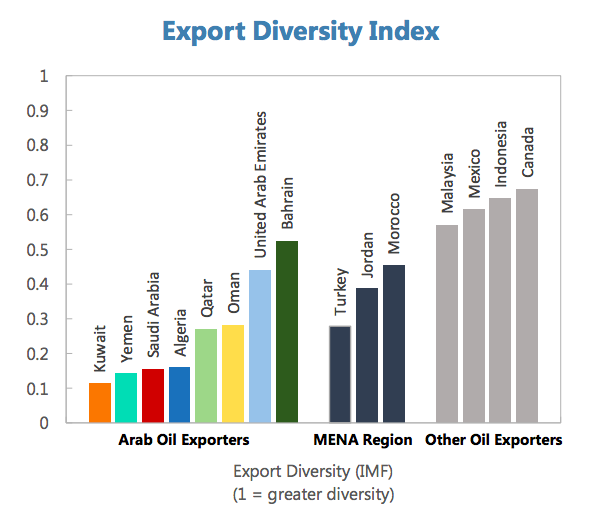

According to Exhibit 2, Countries like Bahrain have a Tax revenue at 1.07% of their GDP compared to the world average of 14.938% of GDP (cited in World Bank, 2013) which poses a question about the sustainability of the hydrocarbon industry as the MENA region’s main source or revenue and the lack of export diversity is unanticipated. Kuwait, from the Gulf Cooperation Council countries, has the least Export Diversity according to the IMF (See Exhibit 3) with 90% of their government revenue collected from crude oil alone (cited in CIA, 2018). Further, the price volatility within the hydrocarbon sector from $42 in Jan 2009 to $125 in May 2011 makes the industry an unreliable source of government revenue (cited in Resilience in a time of volatility, 2015).

Exhibit 2: The comparison between Tax Revenue as a percentage of GDP of the World and Bahrain. Source: World Bank

This paper focuses on the sources of government revenue within the Middle East and North African (MENA) region and proposes the implementation of a regional tax reset through increased taxation and tax reforms, deregulation in the private sector and economic diversification to reduce macroeconomic volatilities caused by the hydrocarbon industry.

Exhibit 3: Export Diversity Index of the Arab Oil Exporting Countries, the MENA region and other Oil Exporters. Source: IMF

Introduction

‘Little else is requisite to carry a state to the highest degree of opulence from the lowest barbarism, but peace, easy taxes, and a tolerable administration of justice’- Adam Smith

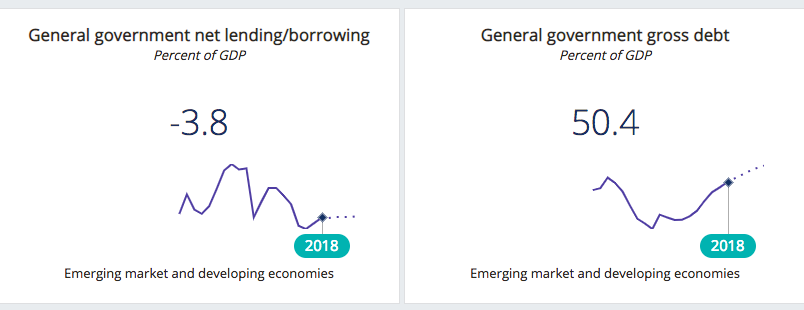

The MENA Region has suffered from a low tax rate primarily due to alternate sources of government revenue in the hydrocarbon industry; inefficient tax collection systems, illicit financial flows, and capital flights also significantly contribute towards the low tax revenue to GDP percentage. However, considering that the government revenues are the ‘lifeblood of modern states’, as the IMF Managing Director, Christine Lagarde describes it, administering sound fiscal measures is of significant importance to improve access to public goods and increase growth rates (cited in Lagarde, 2016). However, with increasing gross government debt and simultaneously falling government borrowing (See Exhibit 4), emerging countries are restricted to raising their tax rates to accommodate for increased public expenditure.

Exhibit 4: General government Net Lending and gross debt trends in 2018 Source: IMF World Economic Outlook October 2018

While a modification of the taxation regime seems like a viable solution, a shift in the system is not necessarily indicative of an increase in government revenue. In some instances, this dissonance can be attributed to inefficient tax revenue collection methodologies, tax inertia (cited in Jones, 2010) and corruption. According to the Corruption Perception Index, 19 of 21 Middle Eastern Countries are below 50; the countries are ranked on a scale from 1, as least corrupt, to 180 being the most corrupt. 4 of the 21 states are in the bottom 10 of the list as the highest perceived corrupt countries in the world (cited in Corruption Perception Index, 2017).

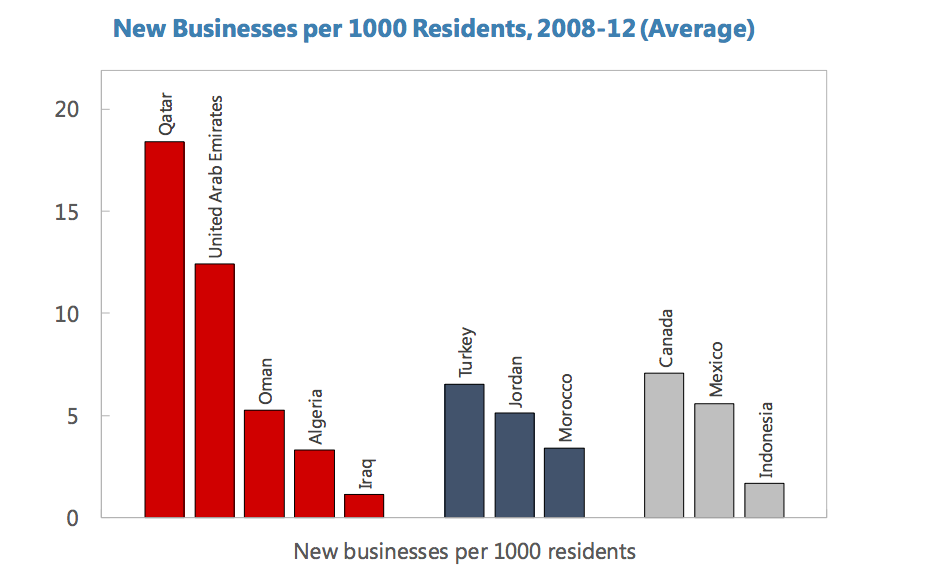

In addition to widespread corruption, following the Arab Spring, unemployment has been rising against an increasing number of youth entering the labor force. The World Bank estimated that 6 million new jobs need to be created each year to absorb the rate of unemployment and can only be combated by increasing the size of the private sector (cited in What’s Holding Back The Private Sector In MENA?, 2016). However, the private sector in the countries within the MENA region is small (See Exhibit 5) due to high regulation within industry.

Exhibit 5: The number of new businesses per 1000 residents in oil producing countries. Source: World Bank Enterprise Surveys

With an increase in the size of the labor force, countries in the MENA region can receive greater returns on taxes and will manage to diversify the stream of incoming revenue. Further, deregulation in the private sector will increase integration into the international markets, increase entrepreneurship and jobs with these countries; corporation taxes can also be levied on private companies. An increase in the taxes is also likely to increase accountability to the people and could mitigate the problem of corruption in the long run. However, in order to understand these solutions, past trends need to be analysed in greater depth.

Taxation Trends in the MENA Region

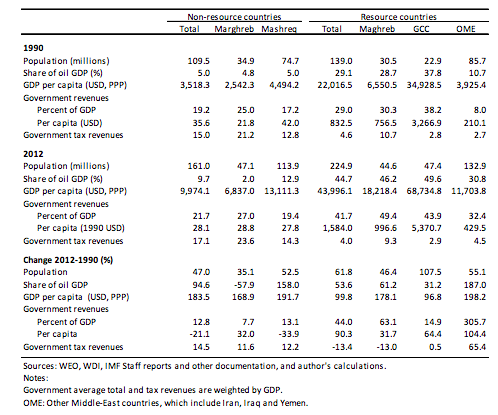

The MENA region is one of the most diverse regions in the world with countries varying significantly in the level of natural resources, political systems, economic systems, and socio-political ideologies. This diversity makes a generalization of tax reform across the region more challenging and a smaller subset of countries need to be considered. The Marghreb region refers to North African countries like Morocco, Libya, and Algeria and has higher tax revenues while the Mashreq countries (Middle East) include countries like Saudi Arabia and UAE and have lower tax revenues and higher oil revenues. According to Exhibit 6, the share of oil as percentage of GDP exceeds 37% in 1990s and 49% in 2012 for the Gulf Cooperation Council (GCC). Tax reforms in the Mashreq region is necessary to diversify revenue sources and to buffer the economic shocks brought about by the volatility of the industry.

Exhibit 6: The distribution of GDP in oil from Margreb and Mashreq countries. Source: WEO and IMF

However, a background of the established tax systems is beneficial in understanding and mitigating these problems. Historically, the greatest sources of tax revenue in the Middle East came from hydrocarbon revenues; this allowed the Mashreq region to have some of the lowest tax revenues globally with countries like the United Arab Emirates having no income taxes altogether. The UAE and Qatar are also world leaders as the easiest countries to pay taxes in globally (PwC, 2017). However, volatility in the industry has lead to the MENA governments recognizing the need to diversify their sources for tax revenues (Iman and Jacobs, 2007). The imminent decline of the oil industry in Syria and Yemen call for urgent tax reforms. Nonetheless, another significant reason for low tax revenues is the institutional corruption in the Middle East and other developing countries in Sub-Saharan Africa (Iman and Jacobs, 2007).

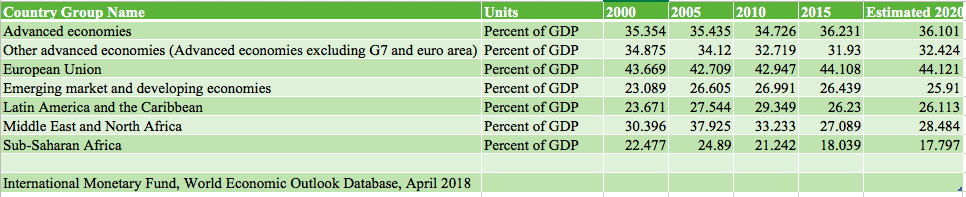

According to Exhibit 7, the IMF estimates that the Tax to GDP ratio is increasing globally from 2000 to 2020 excluding the negative trend depicted for the MENA region and Sub-Saharan Africa. This reduction in Tax/GDP ratio in the MENA region can partially be explained through increased reliance on the hydrocarbon industry, external economic shocks, high levels of corruption in government, heightened internal political tensions brought forth by the Arab Spring and geopolitical pressures in the Middle East.

Exhibit 7: The estimated and actual change in Tax Revenue as a Percent of GDP from 2000 to 2020. Source: IMF

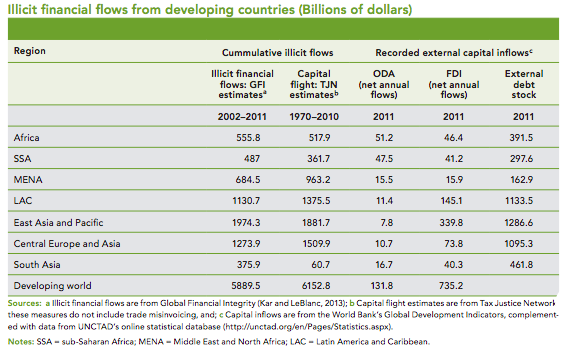

Base Erosion and Profit Shifting (BEPS) by multinational companies also significantly contributes to the reduction in tax base across the MENA region. The OECD defines BEPS as ‘tax avoidance strategies that exploit gaps’ in tax legislations to redirect profits to ‘low or no-tax’ locations (cited in BEPD, n.d.) According to Christian Aid (cited in Ndikumana, 2014), profit shifting practices by multinational corporations (MNC) account for $160 billion in corporate tax losses to developing countries each year, which significantly exceeds the cumulative aid received by all developing countries. The Tax Justice Network, in x, estimates a loss of $963.2 billion between 1970 and 2010 in the MENA region, and a loss of $684.5 billion dollars due to illicit financial flows between 2002 and 2011 alone. The developing world, consisting of the MENA region, South and East Asia and Africa, has witnessed a net loss of $6152.6 billion between the years of 1970 and 2010 to capital flight according to the IMF (See Exhibit 8).

Exhibit 8: The Illicit Financial Flows from Developing Countries. Source: Tax Justice Network

Over 100 countries are currently working together with the OECD countries to find an effective solution for BEPS. Nonetheless, the more stringent laws on corporate taxation can reduce the problem of profit shifting and diversify the sources of revenue within the MENA region while simultaneously increasing the Tax to GDP Ratio and bringing them closer to the global average.

Why does the MENA region need Tax reforms?

With some of the lowest tax efficiency in the region, the MENA countries have low domestic savings rates of less than 15% of their GDP causing a significant funding gap; most countries at this stage of development need a savings rate of 30% of their GDP to achieve a greater degree of economic reform. The Brookings Institute estimates a funding gap of $230 billion in the region; if financed externally, these developing countries will face significant current account deficits and macroeconomic flux. An increase in tax revenues through reduced profit shifting and a greater tax base can increase the government earnings and development can be funded internally.

According to the World Bank, higher revenue administration correlates to a higher perception of corruption; this trend is stark in MENA region. If there is increased transparency and simplification of the process within the tax system, the perception of corruption is likely to reduce. However, the correlation doesn’t necessarily indicate causation.

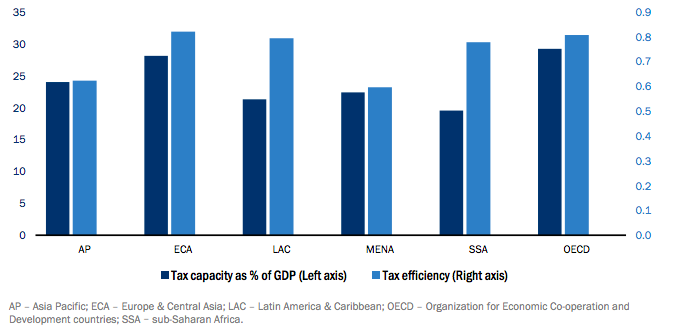

Since the MENA region is functioning on a 20% Tax/GDP ratio according to Exhibit 9, increasing the tax capacity and greater efficiency in the mobilization of revenue in the region can increase the Tax/GDP ratio by 4% (Coulibaly and Gandhi, 2018). Coulibaly and Gandhi from the Brookings Institute also argue that strengthening the tax regime can ‘mobilize $110 billion annually over the next 5 years.’ This sum is greater than the $44 billion aid offered to the entire region and covers almost a half of the ‘financing gap’ and accounts for 17% of the total GDP of the MENA region.

Exhibit 9: Tax Capacity and Efficiency as a percent of GDP. Source: World Economic Outlook 2018

A Case Study: Georgia Tax Collection System: A successful reform

In order to implement a successful tax reform, the MENA region can replicate strategies that have been effective in other countries. Georgia has successfully achieved one of the most effective revision of their existing taxation regime and this case study highlights the changes Georgia and 4 other countries have made.

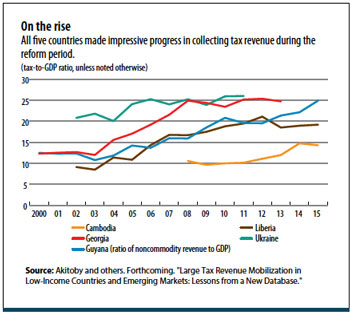

Exhibit 10, cited in Akitoby 2018, depicts the trend of five low-income, emerging economies that achieved successful tax reforms between the years of 2000 and 2015; these countries included Cambodia, Liberia, Ukraine, Georgia, and Guyana. Of the five countries, Georgia had the most significant increase from 12% to 25% Tax Revenue to GDP ratio within the time frame (Akitoby, 2018). Before the reforms, corruption, tax evasion and theft of government funds reserved for public spending were rampant and parallels can be drawn to the MENA region. However, following the Rose Revolution in 2003 in Georgia, rallies for better governance and reduced corruption, new governments in Ukraine, Liberia and Georgia implemented wildly successful tax reforms (Chollet and Gordon, 2005).

Exhibit 10: The change in Tax-to-GDP ratio of Liberia, Cambodia, Georgia, Guyana and Ukraine between 2000 to 2015. Source: Akitoby 2018

Georgia’s new government mandated a no tolerance for corruption policy; in 2004, they passed a revised tax regime which simplified the system, reduced tax rates and eliminated low return taxes which had high monitoring costs. Progressive tax rates between 12% to 20% were replaced with a 20% flat income tax rate to mitigate tax rate negotiation and the social security tax was eliminated altogether (Akitoby, 2018). The revenue losses were compensated through stricter law enforcement and a broader tax base preventing base erosion and profit shifting (BEPS). This was supplemented by electronic tax systems that increased the ease of use and reduced corruption within the system and lowered capital requirements to start new businesses increasing the revenue generated through taxes. They also installed a new system for sharing information across tax authorities, banks and taxpayers through e-filing facilities. These structural changes accounted for 2.5% of the Georgian Gross Domestic Product.

While Georgia’s tax reforms were being implemented, countries like Djibouti and Lebanon also imposed a top tier personal income tax at 25% on people whose income is ten times higher than their respective GDP/Capita. These examples can pave a path of tax reform in the MENA region to increase revenue mobilization and mitigate base erosion.

Proposed Solutions for the MENA Region

Considering that the main purpose of tax reforms in the MENA region is raising the revenue threshold and diversifying sources of revenue, countries that do not impose income tax on their residents including the United Arab Emirates can adopt a flat tax rate of 5%. While significantly lower than most countries, this allows government officials to track the increase in revenue and adjust their tax regimes accordingly. Alternatively, they can consider taxing existing corporations, include capital earnings (Coulibaly and Gandhi, 2018) and tax other non-wage incomes. Since compliance is likely low and capital flight is expected in countries with high levels of corruption, staggering tax reforms over time will be beneficial. Further, with expanding labor forces across the region and the volatility of oil prices, implementing a renewed taxation regime will increase the tax base and reduce current account deficits.

Nonetheless, changing policies without uniform compliance and enforcement is futile. Many countries in the Mashreq region including Saudi Arabia, Libya, and Sudan enforce taxes on expatriates without taxing citizens. Enforcing an effective tax regime on every level prevents profit shifting and increases revenue mobilization. The MENA region can follow Georgia’s stance against corruption, simplify the process and increase transparency. While transparency can also be externally enforced through the creation of a nonpartisan body, sovereignty of the governments shouldn’t be violated.

Further, in order to create jobs for the working age population, governments should deregulate the private sector and encourage startup culture. This can be achieved through subsidies for new enterprises, tax deductions, or awareness campaigns. The increase in private companies in diverse sectors is also likely to increase economic diversity and provide multiple revenue streams into the MENA region.

Conclusion

Having one of the most diverse with socio-economic landscapes, the MENA region should consider implementing effective tax reforms to prevent volatility in their local markets. An active private sector is also likely to improve the GDP of the country in the long run and act as a supplementary source of revenue through economic diversification. While the proposals provide a perspective on the revenue mobilization problem in the region, economies are complex and can be unpredictable. However, economic diversification reduces the risk of economic downfalls and the MENA region should consider alternate methods.

Bibliography

Akitoby, Bernardin. "Raising Revenue." IMF. March 2018. Accessed November 25, 2018. https://www.imf.org/external/pubs/ft/fandd/2018/03/akitoby.htm.

Chollet, Derek, and Philip H. Gordon. "Georgia: Don't Let the Rose Revolution Wilt." Brookings.edu. July 28, 2016. Accessed November 25, 2018. https://www.brookings.edu/opinions/georgia-dont-let-the-rose-revolution-wilt/.

Coulibaly, Brahima, and Dhruv Gandhi. Africa Growth Initiative. October 2018.

Effect of Corruption on Tax Revenues in the Middle East, Patrick A., and Davina F. Jacobs. "Effect of Corruption on Tax Revenues in the Middle East." IMF. November 2007. https://www.imf.org/external/pubs/ft/wp/2007/wp07270.pdf.

"IMF Datamapper." IMF. Accessed November 25, 2018. https://www.imf.org/external/datamapper/datasets/WEO/5.

Jones, Damon. "Inertia and Overwithholding: Explaining the Prevalence of Income Tax Refunds." NBER. May 06, 2010. Accessed November 25, 2018. https://www.nber.org/papers/w15963.

Lagarde, Christine. "Revenue Mobilization and International Taxation: Key Ingredients of 21st-Century Economies by IMF Managing Director Christine Lagarde." IMF. Accessed November 25, 2018. https://www.imf.org/en/News/Articles/2015/09/28/04/53/sp022216.

Mansour, Mario. "Tax Policy in MENA Countries: Looking Back and Forward." IMF. May 2015. https://www.imf.org/external/pubs/ft/wp/2015/wp1598.pdf.

Ndikumana, Léonce. "International Tax Cooperation and Implications of Globalizationi." The United Nations. https://www.un.org/en/development/desa/policy/cdp/cdp_background_papers/bp2014_24.pdf.

"Online Library of Liberty." The Revolutionary Writings of Alexander Hamilton - Online Library of Liberty. Accessed November 25, 2018. https://oll.libertyfund.org/quote/436.

PwC. "The Middle East Has the Least Demanding Tax System, but New Data Highlights Post–filing Challenges, Says PwC." PwC. 2017. https://www.pwc.com/m1/en/media-centre/2016/press-releases/paying-taxes-2017-middle-east.pdf.

"Report for Selected Country Groups and Subjects." IMF. Accessed November 25, 2018. https://www.imf.org/external/pubs/ft/weo/2018/01/weodata/weorept.aspx?sy=2000&ey=2018&sort=country&ds=.&br=0&pr1.x=44&pr1.y=9&c=001,110,123,998,200,903,205,406,603&s=GGR_NGDP&grp=1&a=1.

Riskjell, Ole K. "A Fundamental Tax Reform in Norway." NORWEGIAN SCHOOL OF ECONOMICS. https://brage.bibsys.no/xmlui/bitstream/handle/11250/221033/Masterthesis.pdf?sequence=1.

Further links:

https://www.imf.org/external/np/pp/eng/2016/042916.pdf

https://www.weforum.org/agenda/2017/04/which-countries-are-worst-affected-by-tax-avoidance/

https://data.worldbank.org/indicator/GC.TAX.TOTL.GD.ZS

https://www.cia.gov/library/publications/the-world-factbook/geos/print_ku.html

https://theodora.com/wfbcurrent/bahrain/bahrain_economy.html

https://www.transparency.org/news/feature/corruption_perceptions_index_2017

https://data.worldbank.org/region/middle-east-and-north-africa

https://www.weforum.org/agenda/2017/04/which-countries-are-worst-affected-by-tax-avoidance/

https://www.imf.org/external/np/pp/eng/2016/042916.pdf

http://www.eib.org/attachments/efs/econ_mena_enterprise_survey_en.pdf