Think Complexity Economics is too Complicated? Then this is for you.

Exploring Economics, 2023

First, what is economics?

The answer depends on what perspective you take. However, a very general explanation of economics might be that it is the study of how people use their capabilities and physical environment to satisfy their needs. This definition is very broad, each perspective of economics will give a more specific and slightly different answer.

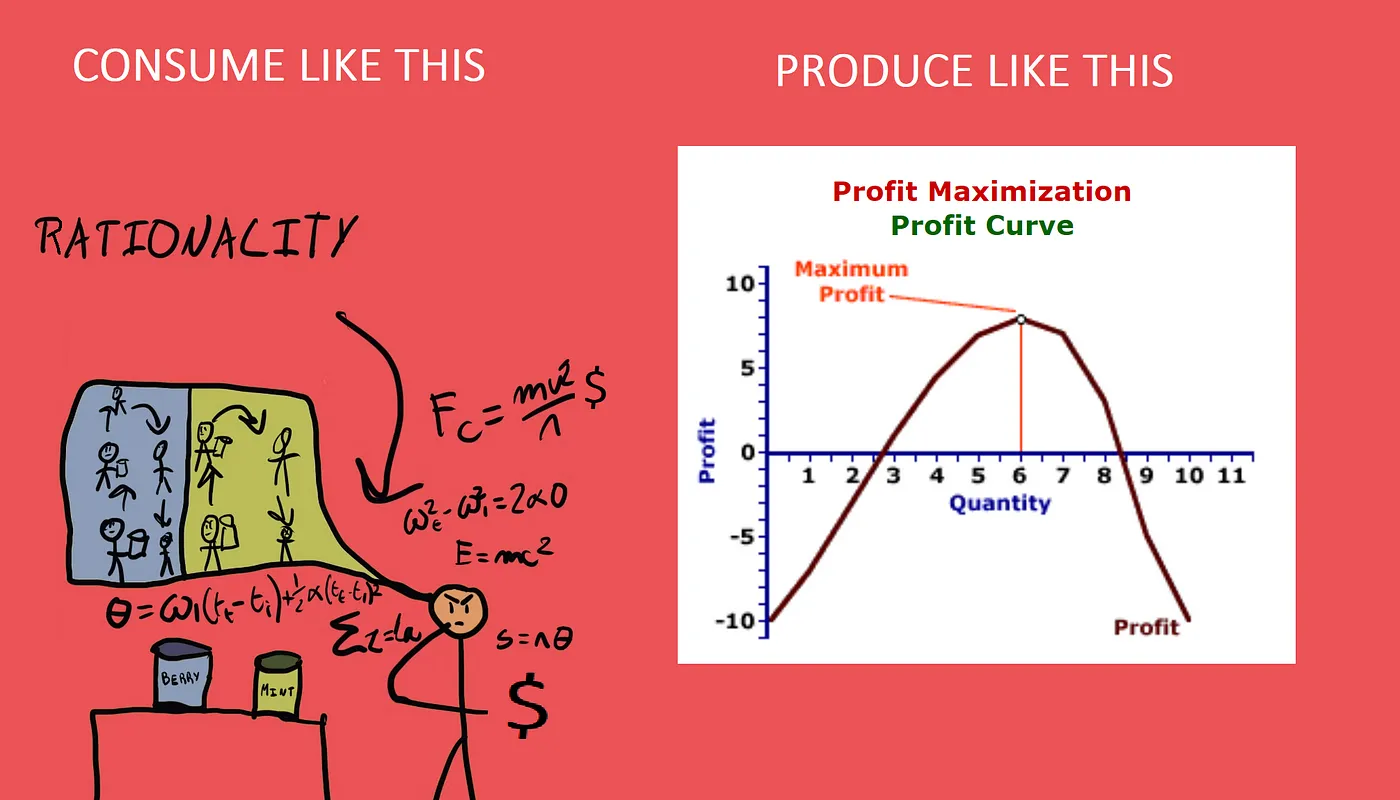

For example, during high school and in most undergrad courses, students learn to see economics from a perspective called neoclassical economics, which focuses on optimization and rational behaviour.

Figure 1: Neoclassical consumption and production (Venter, 2023)

Since each perspective sees the economy in its own way, it also uses its own preferred concepts and methods to study the economy. Neoclassical economics uses methods like graphs and linear equations as seen in figure 1 above. Consumption behaviour is taught by assuming rational choice, and production is always motivated by profit maximisation.

So, what is complexity economics?

Complexity economics is one of these perspectives. It sees the economy as a system that is a part of a larger system and consists of smaller parts that can be treated like subsystems. It tries to study these, how they change, why they change, and what the results of the changes are.

By the way, the type of system described above is called a ‘complex system’, it is where complexity economics gets its name from.

Let’s talk about some concepts and methods that are used by complexity economics to understand complex systems.

1. Value

Value is defined more broadly in complexity economics. It is not just in money or the number of products as in the drawings above. Instead, value is found in networks. For example, social value is found in social networks, financial value flows in financial networks, and ecological value comes from ecological networks.

People often make trade-offs between values of different types without assigning a specific number to it or calculating it (Systems Innovation, 2015). For example, someone may consider a lower-paying job because of some other type of value they receive from doing it, may purchase cruelty-free products as it has environmental value to them, or may visit a certain restaurant because it makes them feel happy.

Measuring this type of ‘value’ is tricky because it depends on context and is created by the interactions of many variables that work together (Systems Innovation, 2015). Soon we will look at some methods that complexity economics uses to help with modeling situations where this type of value is present.

2. Interactions

In our pursuit of the things we value, and for organizations to create value, we interact with each other and with the environment around us. The global economy is one big network connecting not only the interactions of billions of people performing different specialized functions but also the cultural and ecological system (Arthur, 2013). The idea is that complexity economics would be able to work with all of these interactions, not just the ones which were traditionally thought of as falling within the ‘borders’ of the economy (Grabner, 2016).

3. Institutions

With so many interactions, the ones which are often repeated will produce some enduring patterns. Repeating interactions become solidified in economic and social institutions.

Institutions are stable, valued, recurring patterns of behaviour (Huntington, 1996). These may be accompanied by physical structures like banks and shops or they could be mechanisms of social order like democracy or markets.

Institutions determine the behaviour of a group of individuals and facilitate interactions by defining certain rules. Sometimes the rules are written down, other times it is deep in our culture and we don’t even know we are following them (North, 1990).

Although complexity economics is not the first to bring these ideas of institutions into economics (institutional economics is), complexity economics can bring these ideas into the heart of its models ,as you will see in the last section of this article.

4. Feedback loops

Cycles emerge whereby our actions create new institutions, these new institutions then facilitate our interactions, and from the new interactions emerge new institutions. This is an example of a feedback loop. You will see more examples of feedback loops in the sections below and how feedback loops are used to model situations in the real world.

Feedback loops is a term used by physicists and mathematicians, some of the founders of complexity economics were physicists. However, the general idea of ‘feedback loops’ is much older. It is known as ‘cumulative causation’ and Thorstein Veblen (The guy who founded institutional economics) was the first to talk about it as a way of thinking about economics.

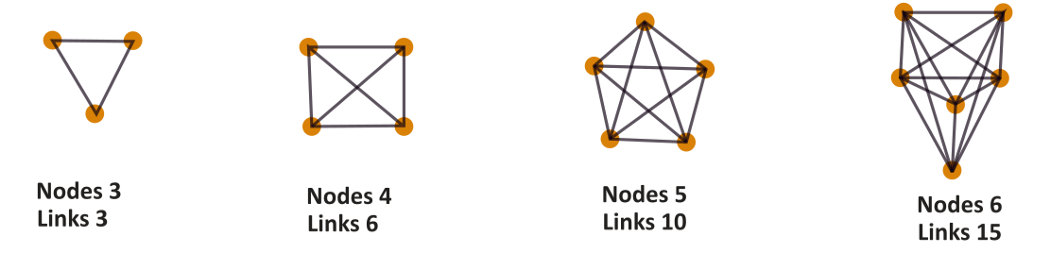

5. Networks

People and organisations are embedded in overlapping networks. These include social networks, cultural networks, technological networks, production networks, consumption networks, financial networks, and many other types of networks.

Resources flow through these networks. How these resources become available to us depends on where we lie in the network as well as the structure of the network itself.

The value (see 1 above) flowing through the network may increase exponentially every time a new person or organisation joins and the number of possible interactions among them, too. As can be seen in Figure 2 below.

Figure 2: Nodes and links in a network (Venter, 2023)

(Note that a node does not necessarily have to be connected to every other node, figure 2 merely shows the potential number of links.)

Value is something that emerges from the network connections. The value of the total network is higher than the value of each part on its own.

For example, if enough people think of being an economist as a socially respected job, the job gives them access to a culturally valuable identity. If someone joins LinkedIn but nobody is on it, it has no value, the more people are on LinkedIn the better. A positive feedback loop (see 4 above) may come into existence where more people join, increasing the value of a network, causing even more people to join.

Billions of actions of different firms are coordinated in the types of networks discussed above. This results in complex services and products that no one person or organisation can perform or create by themselves individually (Jackson, 2010).

6. Open systems & Closed systems

Open systems are so integrated with other systems that they cannot be defined by their boundaries (Bertalanffy, 1988). Studying the economy as a complex system implies that we see it as an open system that cannot be studied as separate from other systems like the cultural or ecological system.

On the other hand, closed systems are isolated from other systems. Studying cells under a microscope or using a production function to analyze how factor inputs are related to product outputs are examples of closed systems. Here you cannot see how your subject of inquiry would respond if it were an integrated part of the real world where other systems influence it.

If we see the economy as a closed system, we cannot study what happens when it takes in value from other systems such as social value from the cultural system and ecological value from nature. Neither can we study the influence that the economy has on those systems, for example, how economic systems bring out certain behaviour in people or cause environmental degradation (Arthur, 2013).

7. Non-equilibrium

Closed systems will reach an equilibrium because there are a finite number of variables being considered and because they are shielded from the real world (Arthur B, 2013). For example, a production function will indicate the quantity a company should produce in order to be most efficient or to maximize its profit. However, open systems will not exhibit equilibrium because they are in a constant state of change, being influenced by other systems and influencing these systems in continuous cycles. In other words, inputs and outputs change as the whole system changes (Farmer and Geanakopolos, 2009).

Unlike standard economics which is based on equilibrium from modeling the economy as a closed system, complexity economics sees the economy as an open system that is never in equilibrium.

8. Algorithms and equations

Closed systems use linear equations while open/complex systems are modeled with algorithms which are then put into code and run by a computer. These simple rules or algorithms can then create complex interactions and emergence.

When computers run these algorithms, it produces a simulation of the real world. You can see some of these examples in the last section of this article.

9. Emergence

Emergence describes the ability of individual components of a large system to work together to give rise to dramatic and diverse behaviour. Parts of a system do things together that they would not do alone. For example, individuals self-organising into neighborhoods in cities — all with no leaders or central control, patterns unfold into institutions and cause shifts in our culture, and financial bubbles develop due to individual actions (Holland 2014). It is almost as if the rules of the game are being invented by some unseen force or by the game itself, this is said to be an emergent phenomenon related to self-organisation.

10. Decision making and behaviour

How people and organisations make decisions is a central part of economics and complexity economics. Of particular interest are individual choices in the allocation of resources and how these micro-level actions interact to give rise to macro-level patterns of organisation. (Goodwin et al. 2022)

Since individuals interact in a complex system, they change their actions and strategies in response to the outcome they mutually create (Arthur, 2021).

As far as how people choose, complexity economics is aligned with the idea that people uses mental shortcuts (heuristics) that makes sense in the culture and environment that they are accustomed to and when their choice turns out to be wrong it is due to a misinterpretation or misrepresentation of the situation. These mental shortcuts can give more optimal results than probability theory calculations that neoclassical economics believe people implicitly use.

So in real life, these mental shortcuts may emerge from people being able to interpret nuances in situations over time and learning from experts. Whenever we use our expertise and gut feelings instead of probability equations, we are working with heuristics (Gigerenzer, 2012).

Complexity economists often won’t interpret a wrong decision as a “behavioural bias” or as something that is irrational. Instead, they will interpret a wrong decision as the result of a wrong fit between the heuristic used and the situation, they see it as the most rational choice given the mental toolkit of the decision maker.

For example, choosing which clothes to buy may involve hundreds of options and many decisions that unfold over time as it is dependent on choices taken in the past. What someone does also depends on what they think others might do. People use shortcuts, they think in scenarios and context, and they constantly update their internal decision-making model that is used to make easy work of difficult decisions without the need for considering all outcomes, probabilities and utilities (Systems Innovation, 2015).

11. Time dependence and dynamic vs linear change

The real world is in a dynamic state of change. Models developed by neoclassical economics that describe phenomena with a few lines on a graph are geared toward hypothetical static situations. These will not produce useful results as the whole system evolves over time.

Time influences the way our economy works and the way its parts relate to each other. A model from orthodox economies which explains a static or closed system cannot explain our economy at different times equally well (Robinson, 1980). Instead, complexity economics tries to understand how the complex system itself changes over time.

12. Economic development and growth

Growth itself is not the main concern. Instead, the focus is on development according to the things we value.

Since the economy is seen as a complex adaptive system that evolves over time, complexity economics focuses on the non-equilibrium processes that transforms the economy from within. The focus is on technological innovation and new business models that lead to a process of creative destruction in an economy that grows in a somewhat organic way. The focus is on how changes in one part lead to new opportunities or problems in others as the whole thing evolves with different industries and sectors becoming interdependent (See for example Harvard Growth Labs, 2023). Out of this process of evolution, we get what we might call economic growth, not in the traditional sense of gross output of goods and services but in terms of qualitative structural transformation in becoming more differentiated and integrated to exhibit greater levels of complexity (Systems Innovation, 2015).

For example, note the level of complexity that is required to create some service or a product like a computer. This product or service will then be used in a network and give people access to a better way of doing things.

The way that complexity economics models ‘growth’ will be explained in the last section of this article which presents some applications of complexity economics.

13. Agent-based models and simulations

These are the methods used by complexity economics to get from the micro level to the macro level. Instead of simply getting an aggregate of all the micro variables as if we are dealing with a closed system, it looks at how other systems influence the economy in real-time and try to simulate it with computers to find the rules of these interactions.

Agent-based models and stock flow models are types of computer models where the interactions of diverse autonomous agents are simulated over time (Examples are provided at the end of the article).

14. Complexity theory and Chaos theory

Complexity Theory is the overall study of complex systems. It is not just in economics that we can study such systems. How storms emerge, the way ant colonies work, human evolution, water networks, and lots of other phenomena are examples of complex systems (Kauffman, 1995).

Chaos theory states that within what might appear as random chaos in complex systems, there are actually underlying patterns, interconnection, constant feedback loops, and self-organization (Fractal Foundation, 2019).

15. Borrowing from other disciplines

Many scholars feel that complexity economics is just a methodology and point to the fact that we still need theories of the environment and psychology on which to build the rules of the algorithms. Thus, complexity economics can gain a lot by borrowing from the deep perspectives found in institutional economics, behavioural economics, and ecological economics (Grabner, 2016).

What are some applications of complexity economics?

Since the financial crisis in 2008, mainstream equilibrium models have had little to add in terms of policy direction (Armstrong, 2017), there has been increasing interest in using methods from complexity theory (Battiston et al, 2016).

1. Trading methods

As Arthur (2021) explains, the standard neoclassical theory of financial markets cannot account for actual market phenomena such as the emergence of a market psychology, price bubbles and crashes, and random periods of high and low volatility.

Researchers at the Santa Fe Institute (SFI) have set up an ‘artificial’ stock market. The ‘investors’ were little artificial intelligent (AI) programs that could differ from one another. Rather than share a self-fulfilling forecasting method, they were required to somehow learn or discover forecasts that work.

These ‘investors’ were free to independently design and test various forecasting strategies, discard any that didn't pan out, and occasionally produce new strategies to take their place. Based on their current most accurate methodologies, they made bids or offers for a stock, and the stock price results from these.

Researchers included an adjustable variable to pre-determine the rate-of-exploration to govern how often these artificial investors could explore new methods. When they ran the simulation, they found two regimes or phases. At low rates of investors trying out new forecasts, the market behaviour collapsed into the standard neoclassical equilibrium. Investors became alike and trading faded away. In this case, the neoclassical outcome holds, with a cloud of random variation around it. However, if the investors tried out new forecasting methods at a faster and more realistic rate, the system goes through a phase transition. The market develops a rich psychology of different beliefs that change and do not converge over time; a healthy volume of trade emerges; small price bubbles and temporary crashes appear; technical trading emerges; and random periods of volatile trading emerge. Phenomena we see in real markets emerges.

This last phenomenon of random periods of high and low volatility happens because, if some investors occasionally discover new profitable forecasting methods, they then invest more and this changes the market, causing other investors to also change their forecasting methods and their bids and offers. These phenomena are the result of economic agents discovering behaviour that works temporarily in situations caused by other agents discovering behaviour that works temporarily.

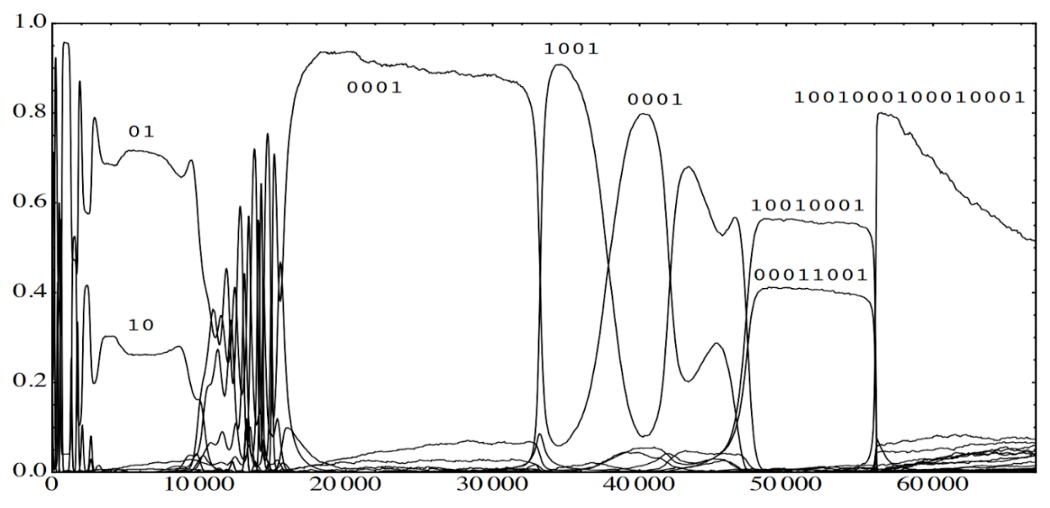

Below is a similar simulation. The horizontal axis represents time and the vertical axis represents how popular a particular strategy is. Over time, strategies evolve based on pressures exerted by other strategies. Strategies also become more complex as represented by the string of numbers above each line.

Figure 2: Computerised simulation (Arthur, 2013)

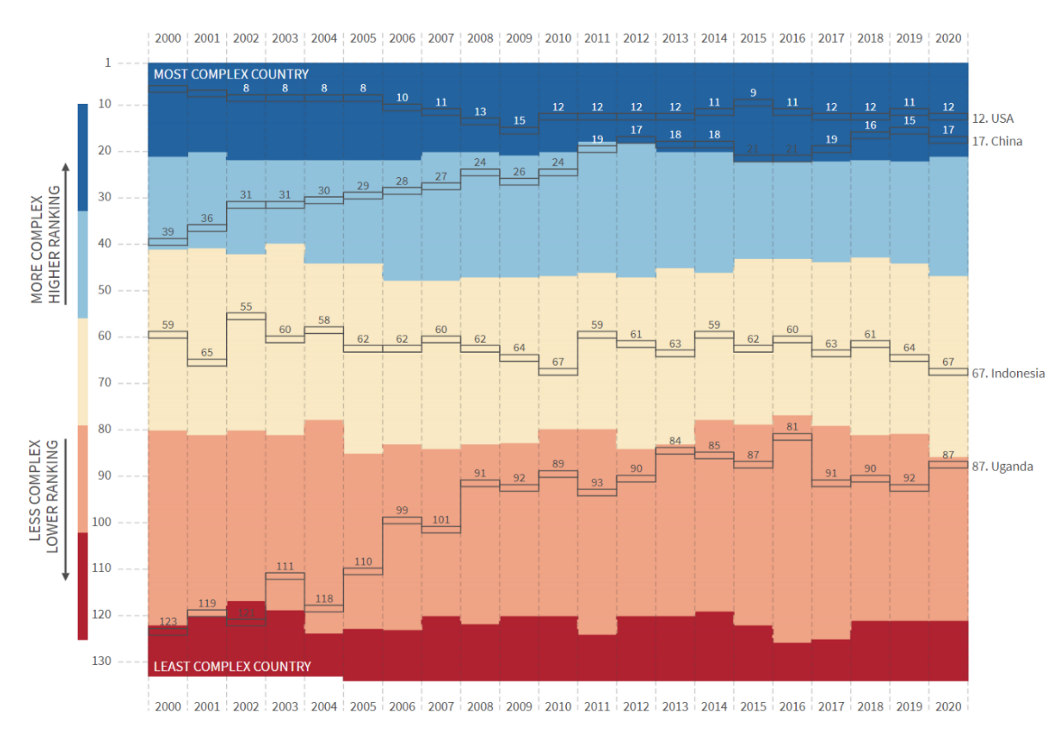

2. Economic complexity

Figure 3: Economic Complexity (Harvard Growth Labs, 2022)

Economic development requires the accumulation of productive knowledge and its use in both more and more complex industries. Harvard Growth Lab’s Country Rankings assess the current state of a country’s productive knowledge, through the Economic Complexity Index (ECI). Countries improve their ECI by increasing the number and complexity of the products they export. The diagram shows how each country’s ECI ranking changed since 1995.

A country’s current ECI and its Complexity Outlook (connectedness to new complex products in the Product Space) is a good prediction of a country’s future growth.

ECI alone helps explain the biggest part of the difference in current income levels between countries (Harvard Growth Labs, 2022).

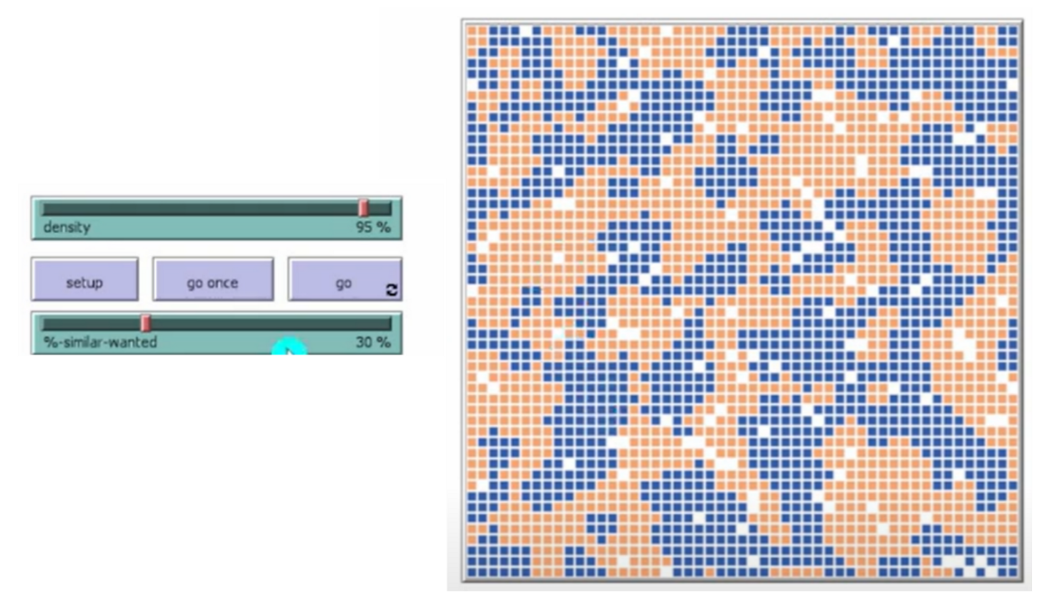

3. Racial segregation in neighbourhoods

Figure 4: Racial Segregation in Neighbourhoods (Centre for Connected Learning, 2010)

This is a simulation of the behaviour of two types of agents in a neighborhood. The orange agents and the blue agents get along with one another. But each agent wants to make sure that it lies near some of “its own”. That is, each orange agent wants to live near at least some orange agents, and each blue agent wants to live near at least some blue agents. With the buttons on the left, neighbourhood density and agent preferences can be set. The simulation then runs to show how these individual preferences ripple through the neighborhood, leading to large-scale patterns of segregation. This model is based on Thomas Schelling’s writings on housing patterns in cities (Centre for Connected Learning, 2010).

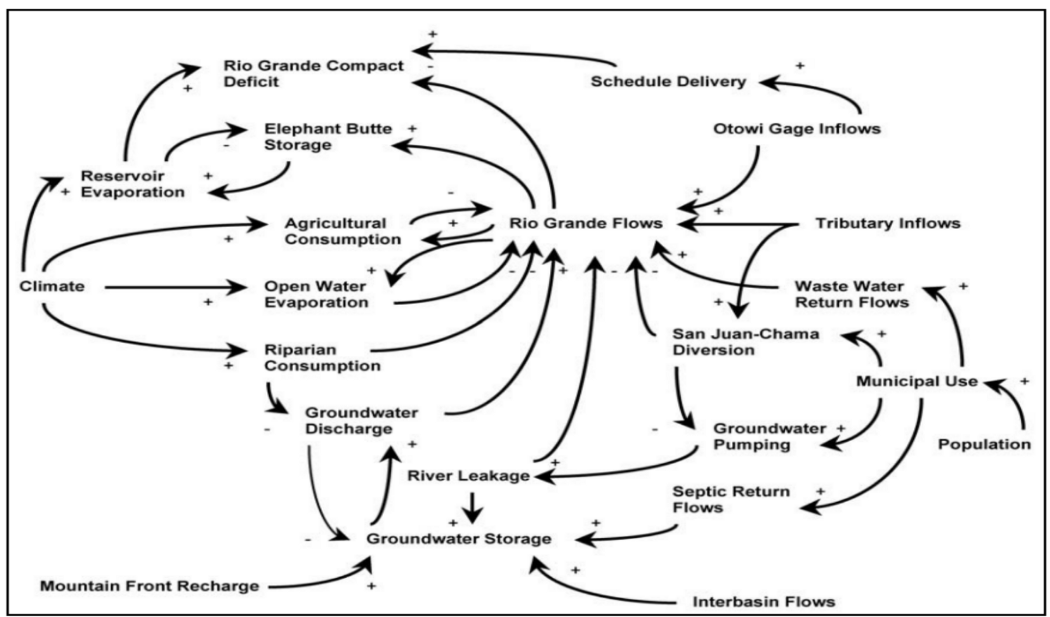

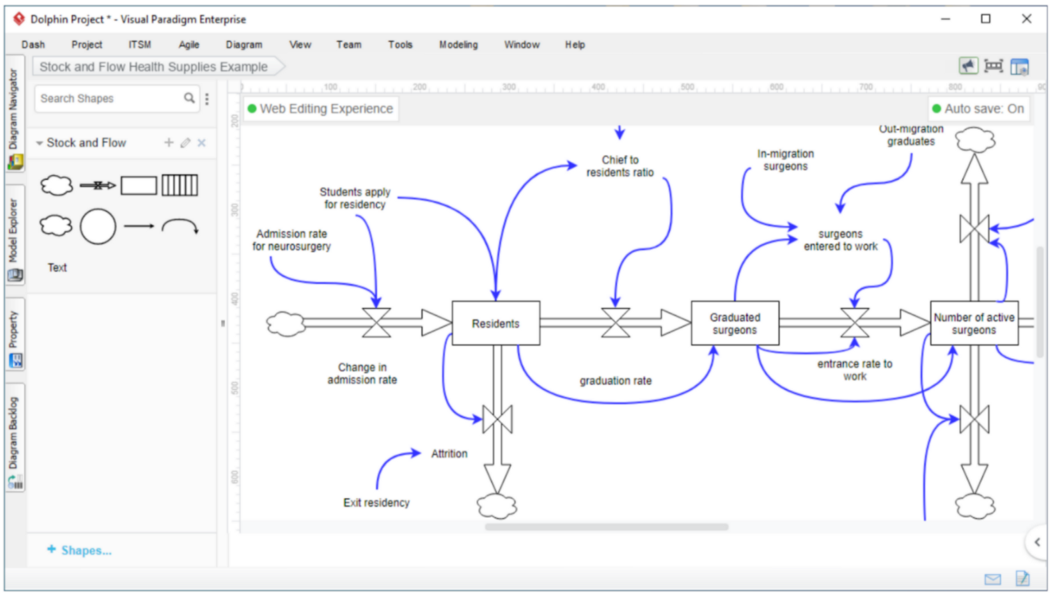

4. Causal loops and stock flow diagrams

Figure 5: Water flows in the Rio Grande basin (Tidwell, et al. 2004)

Figure 6: The flow of skilled employees in a nation (Rafiei, et al. 2018)

Figure 5 shows demand for water in the Rio-Grande region in the USA. It shows the flow of water through industrial and ecological systems, simulating water usage between agents and the ecosystem. Figure 6 shows the factors determining the number of skilled employees (in this case neurosurgeons) within a national boundary. Computer programs assist people in creating such models. These models are known as causal loop diagrams or stock-flow diagrams.

So, what is complexity economics?

Now that we understand the concepts and methods of complexity economics as well as some of its applications, we are ready to grasp the full academic explanation:

Complexity economics is an approach of economics that focuses on the study of complex systems and how these behave over time. It is based on the idea that economic systems are not static and can change in unexpected ways as a result of the interactions between different agents within the system in a time-dependent manner.

Complexity economics recognizes that economic systems are composed of many different agents, such as individuals, firms, and governments, which interact in a nonlinear dynamic fashion. This interaction can lead to the emergence of complex patterns and behaviors that cannot be predicted or controlled in a traditional, linear economic model.

One of the key features of complexity economics is the emphasis on agent-based modeling, which involves simulating the behavior of individual agents within a system in order to better understand how the system as a whole functions. This approach allows economists to study the micro-level interactions between agents and how they contribute to the emergent behavior of the system at a macro level.

Overall, complexity economics seeks to provide a more realistic and nuanced understanding of how economic systems function, and to develop new tools and approaches that can help policymakers (Arthur, 2013).

There is still so much to discover!

In the Discover section we have collected hundreds of videos, texts and podcasts on economic topics. You can also suggest material yourself!

Discover material Suggest material

References

- Armstrong, A 2017 Rebuilding Macroeconomics, accessed 15 January 2023 <https://www.rebuildingmacroeconomics.ac.uk/why-rebuild-macroeconomics/>

- Arthur, B. (2013). Complexity economics: a different framework for economic thought. Santa Fe Institute Working Paper 09-08-032. Retrieved 15 January 2023, https://www2.econ.iastate.edu/tesfatsi/ComplexityEconomics.WBrianArthur.SFIWP2013.pdf

- Arthur, B 2021, ‘Foundations of complexity economics’, Nature Review of Physics, vol. 3, no. 1, p. 136–145. <https://doi.org/10.1038/s42254-020-00273-3>

- Battiston, S., Farmer, J. D., Flache, A., Garlaschelli, D., Haldane, A. G., Heesterbeek, H. and Scheffer, M. 2016. Complexity theory and financial regulation. Science, 351(6275), p. 818-819.

- Bertalanffy, L 1988 General system theory, G. Braziller. New York.

- Center for Connected Learning and Computer-Based Modeling, 2001, Netlogo model of ethnocentrism. Accessed 20 November 2022. https://ccl.northwestern.edu/netlogo/models/Ethnocentrism

- Farmer J.D, Geanakoplos J, 2009 ‘Non-Equilibrium Economics and Agent-Based Models’, Complexity, Vol. 14, No. 3, p. 11-38. https://doi.org/10.1002/cplx.20261

- Gigerenzer, T. 2012. Ecological Rationality: Intelligence in the world. Oxford University Press, USA

- Goodwin N, Harris J, Nelson J, Rajkarnikar P, Roach B (2022) Microeconomics in Context, Taylor and Francis Ltd, Boston.

- Gräbner, C 2017, ‘The complementary relationship between institutional and complexity economics: The example of deep mechanismic explanations’, Journal of Economic Issues, vol. 51 no. 2, p. 329-400. https://doi.org/10.1080/00213624.2017.1320915

- Harvard Growth Labs, 2023, Atlas of Economic Complexity. Accessed 15 January 2023. https://atlas.cid.harvard.edu/

- Holland J.H 1999, Emergence from chaos to order, Cambridge, Mass ISBN 978-0738201429

- Jackson, M 2010. Social and economic networks. Princeton University Press. USA

- Kauffman, S 1995, At Home in the Universe: The Search for the Laws of Self-Organization and Complexity. Oxford university press

- North, D. C. 1990. Institutions, institutional change, and economic performance. Cambridge University Press.

- Rafiei S, Daneshvaran A, Abdollahzade S. 2018. Forecasting the shortage of neurosurgeons in Iran using a system dynamics model approach. J Educ Health Promot, 7:16. DOI: 10.4103/jehp.jehp_35_16

- Robinson, J 1980, ‘Time and Economic Theory’, Kyklos, vol. 33, no. 2, p. 219-229. https://doi.org/10.1111/j.1467-6435.1980.tb02632.x

- Huntington, S 1996, Political Order in Changing Societies. Yale University Press.

- Systems innovation. 2015, Value Theory. Retrieved 15 January 2023, <https://www.youtube.com/watch?v=H3SnxnO-5Es&list=PLsJWgOB5mIMCf7yNnXrHrtaBsa7GXqZAs&index=6>

- Tidwell, V.C., Passell, H.D., Conrad, S.H. 2004. System dynamics modeling for community-based water planning: Application to the Middle Rio Grande. Aquat. Sci. 66, 357–372. https://doi.org/10.1007/s00027-004-0722-9

![]()

![]()

![]()

![]()

This content is licensed under a Creative Commons-Licence (CC BY-NC-ND 4.0).